Ambient software

How GenAI and transcription tools are unlocking software adoption in laggard markets.

Over the past three essays, I explored whether GenAI qualifies as a true platform shift. I began this exploration by defining the core elements that characterize a platform shift. I then examined its impact on software development, the emergence of Service-as-a-Software models, and the rise of cross-silo orchestration layers we called “System of Systems”. Each case pointed to a structural change in how value is created, delivered, or monetized.

This article required a separate space. Unlike the previous ones, it doesn’t introduce a new business model but it highlights how GenAI can enhance an existing one. What follows is not about reconfiguring the logic of software companies, but about how a key constraint in Vertical SaaS (vSaaS) may be dissolving, opening new room for adoption where software penetration was historically low.

How GenAI is rewriting the vSaaS playbook

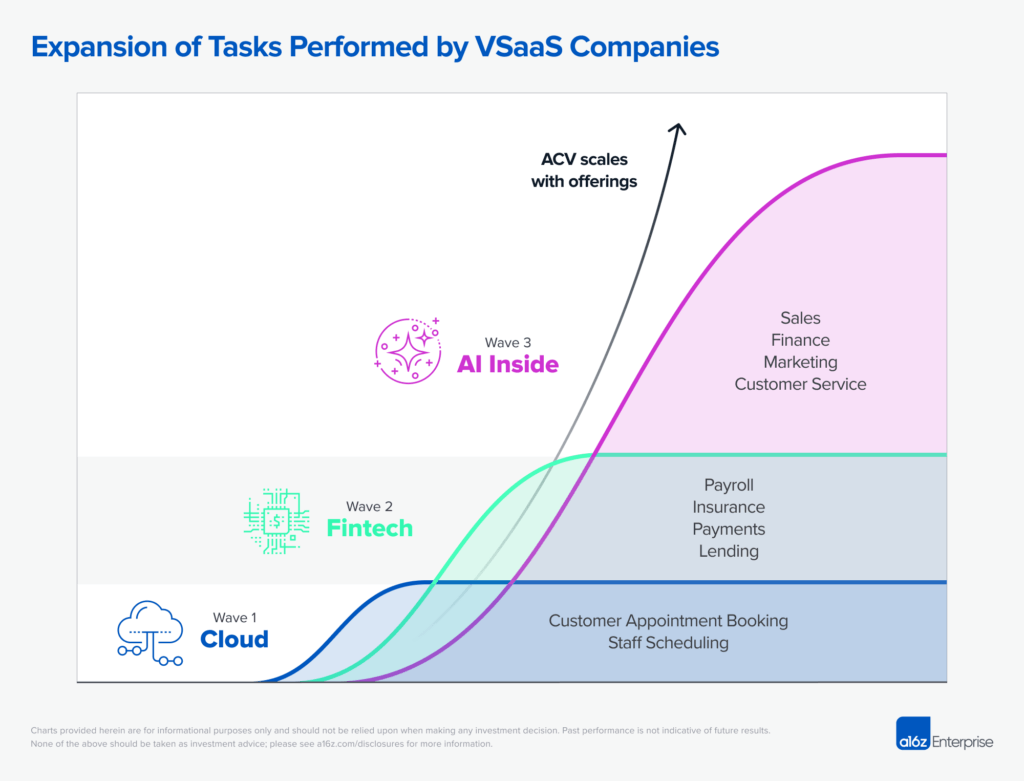

Vertical SaaS refers to software products tailored to the specific needs of a single industry, from restaurants to fitness studios to dental labs. These startups typically start by solving a specific pain point or workflow, then expand their footprint by serving the same audience across adjacent needs. As the product grows into new areas of the workflow, usage deepens, integrations multiply, and trust compounds. For investors, this makes vSaaS especially compelling: once established, the dominant player is hard to displace.

This “Land & Expand” strategy has played out repeatedly in many successful cases and the recent rise of GenAI agents has only reinforced this playbook, making it feasible to automate additional workflows on top of the operating system.

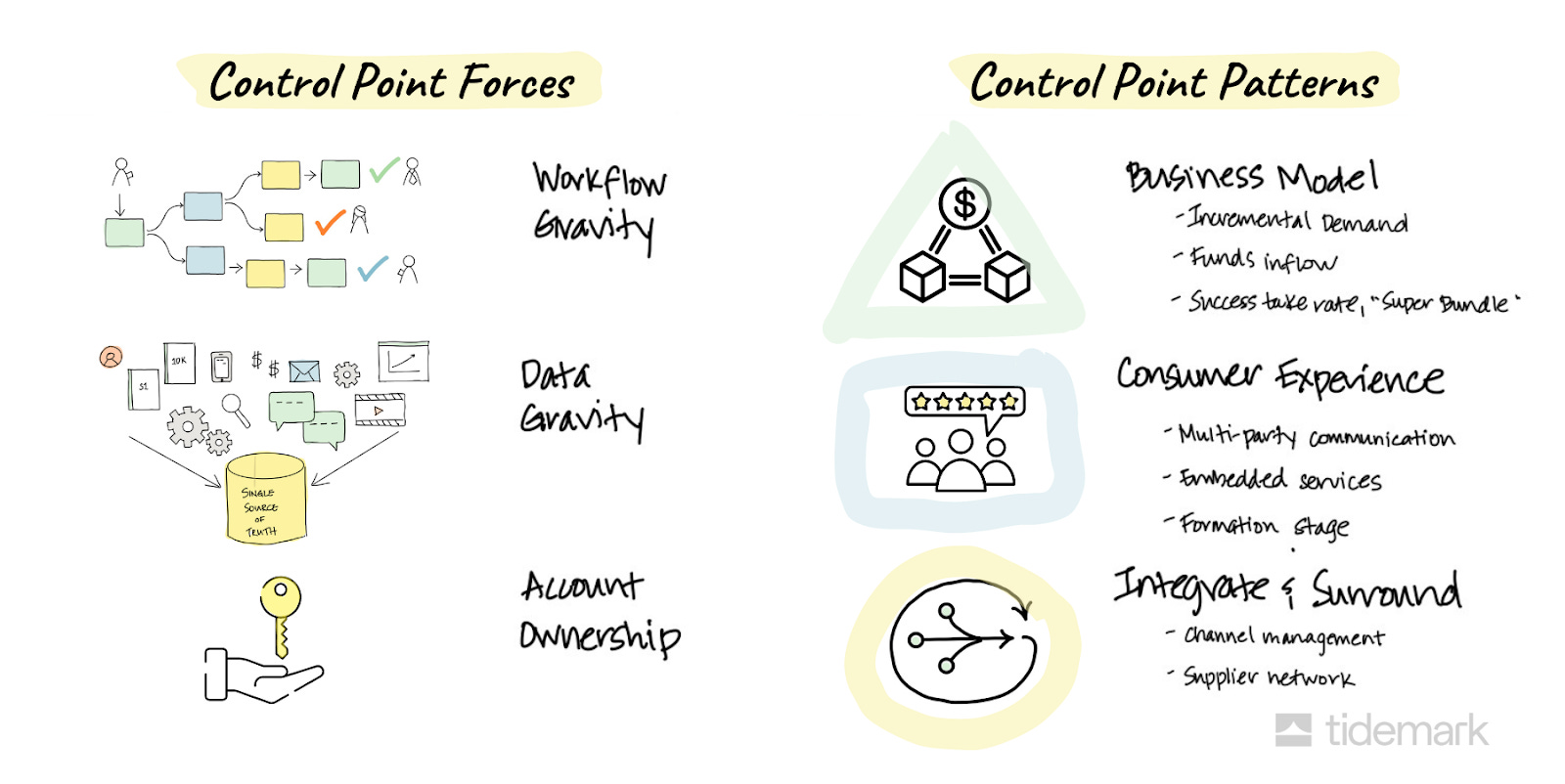

The mechanics behind this expansion are driven by a startup’s ability to conquer what Tidemark defines as control points, the systems that anchor workflows, data, and decision-making within an organization. These control points emerge through different forms of gravity:

Workflow gravity, where users spend the most time and initiate key processes

Data gravity, where the most critical information resides and is hardest to migrate

Account gravity, when the system is owned or championed by the highest-ranking stakeholder

Capturing one or more of these dimensions creates structural leverage and unlocks the right to expand.

What I’ve come to believe is that GenAI doesn’t just amplify existing growth dynamics. It can also serve as the entry point itself. Not just a way to increase ACV, but a way to unlock markets previously out of reach and kick off the vSaaS playbook from scratch.

Why transcript tools are more than note-takers

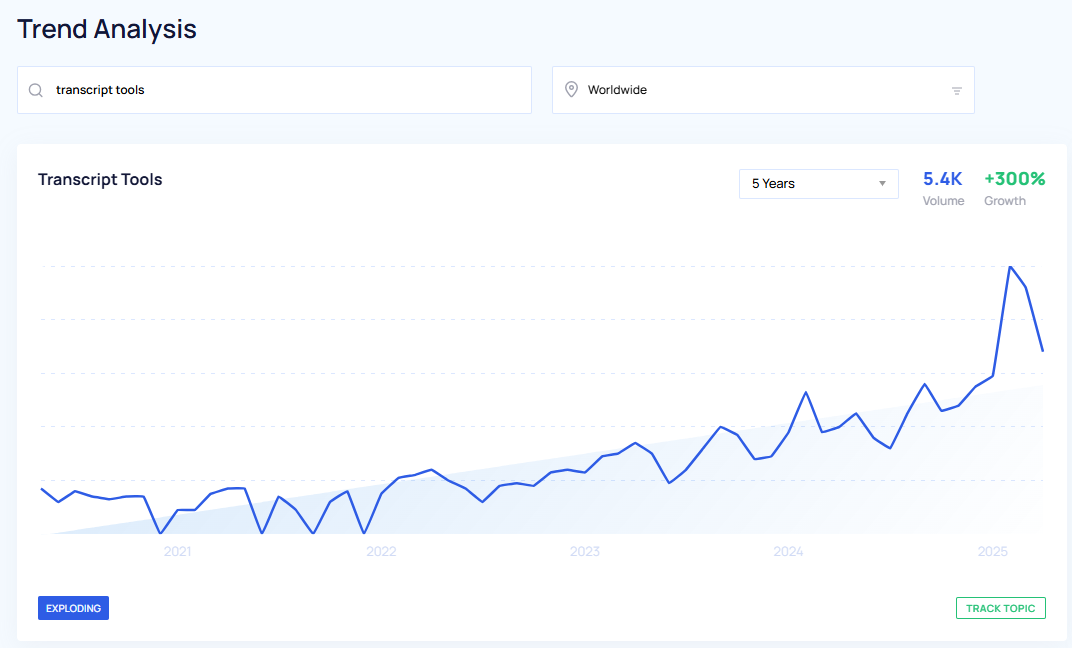

Interest in transcription tools has surged in recent months, driven by a combination of technical breakthroughs and growing user familiarity. What once felt like a niche utility is becoming part of the everyday stack. The recent 20M$ Series A raised by Granola last year is just one signal of this inflection point, reflecting how tools once seen as optional are increasingly moving toward the center of how people work.

While recent advances in speech-to-text systems and large language models have made transcript quality reliably actionable, I believe it’s reductive to frame these tools as simple note-taking assistants. What they enable is far more profound: Transcript tools can now capture, structure, and contextualize interactions with minimal friction, making it possible to create and maintain a system of record with far less effort than just a few years ago.

This reduces the need for manual entry, lowers operational overhead, and reshapes how software fits into the flow of work. What once required a dedicated back office can now be managed through ambient capture and a natural interface to query or update the system.

This shift matters most in sectors that remain largely undigitized and lack structured systems of record. Think of healthcare, agriculture, restaurants, hospitality, manufacturing or legal services. These are what we might call “laggard markets”.

A few recurring patterns tend to define these sectors in my opinion:

Fragmented markets, mostly composed of small companies

People-intensive, hard-to-formalize workflows

Practitioner-led culture, with limited managerial mindset

Offline, high-touch value creation processes

Regulatory friction slowing down digitalization

These traits manifest in two fundamental barriers to digital adoption:

Cultural awareness: If a process doesn’t feel broken, there’s no perceived need to digitize it. End of the game.

Lack of resources (skills and time): Limited digital skills among staff and little capacity to retrain and adapt the organization to new tools and processes.

In my view, AI-native vSaaS can help remove these frictions, especially the second one. By automatically building a dataset where the alternative would have been manual set-up, and by providing a natural language interface to access it, these tools minimize the training required, reduce onboarding and set-up costs, and compress the time to ROI.

In this context, transcript tools becomes more than just a meeting add-on. They become the gateway to unlock greenfield markets, using ambient data capture as the wedge and vertical SaaS as the delivery model. It’s a way to create a company’s first system of record, with a UI/UX that adapts to how people work, rather than forcing them to adapt to the tool.

The next big thing will start out looking like a transcription tool

Transcription is becoming infrastructure in healthcare

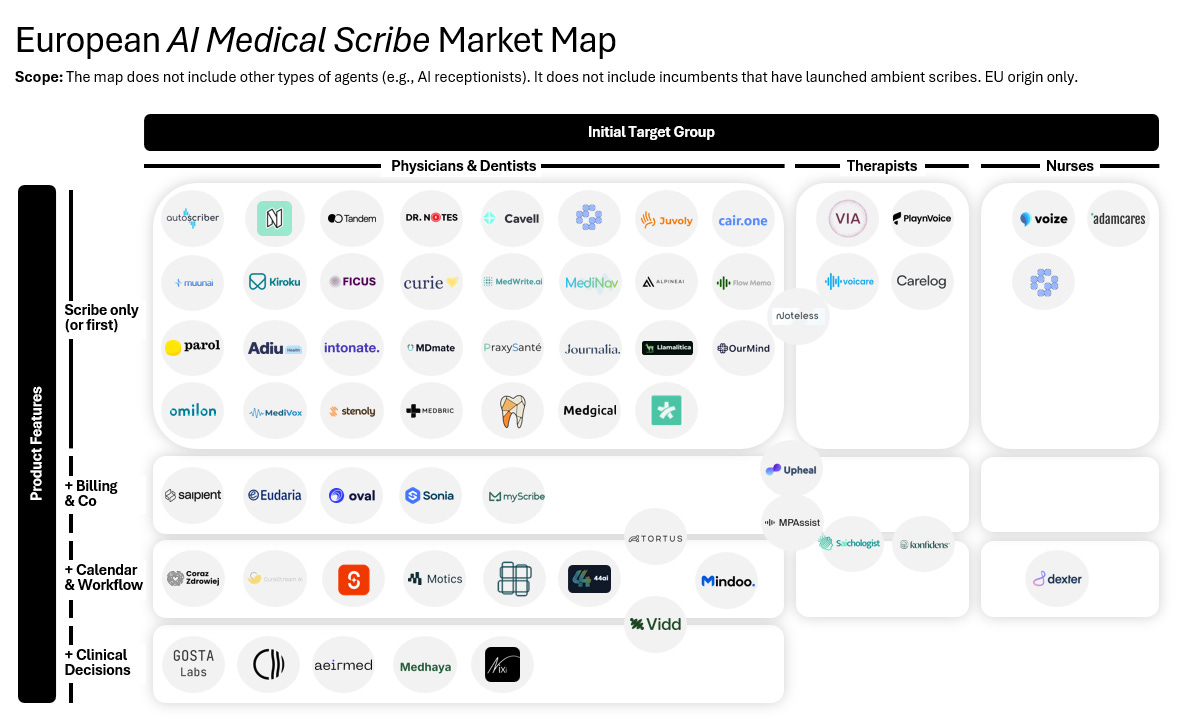

A glance at the recent a16z market map reveals a surge of transcription-based startups across use cases, from healthcare to specific business functions like recruiting or sales.

A particularly interesting example is the rapid rise of AI medical scribes. After an early wave in the US, led by companies like Abridge and DeepScribe, the European market is now following a similar trajectory. Heal Capital recently mapped over 60 active players, spanning diverse customer segments (physicians, therapists, nurses) and functional scope (from basic transcription to billing, workflow, and clinical decision support).

Healthcare organizations, whether hospital chains, public hospitals, or small private clinics, are environments where digitalization has historically struggled to take hold. These markets have long been dominated by legacy vendors founded in the '80s and '90s, offering monolithic EHR and ERP systems. Transcript tools are not just improving workflows; they are creating the conditions for boosting software adoption in the first place.

Challenges remain. Defensibility is a key concern: many medical scribes operate at feature level and may face growing pressure as the underlying technology commoditizes. They also face increasing competition from native transcription features natively embedded in video conferencing platforms like Zoom, Teams, or Google Meet, raising the question of how many tools users are willing to adopt, and where transcription truly belongs in the workflow. At the same time, transcription accuracy remains critical: errors in generated notes can directly impact clinical decisions. Regulation adds another layer of uncertainty. In the UK, AI scribes have now been formally classified as medical devices: most startups operate under class I self-certification, but some are already preparing for class II as a way to build long-term defensibility.

Still, the underlying thesis holds. AI scribes show how ambient transcription can act as the first scalable interface between practitioners and software in laggard markets, reducing setup friction, creating structured data where none existed, and unlocking a path to vertical expansion.

A similar thesis may also apply to voice agents, but that’s a deep dive (maybe) for another article.

If you're building an AI scribe or a vSaaS for laggard markets, I’d love to hear from you. Let’s chat on LinkedIn or write me at boldrini@proximitycapital.it